What is the difference between a construction loan and a home equity loan?

By John Johnson

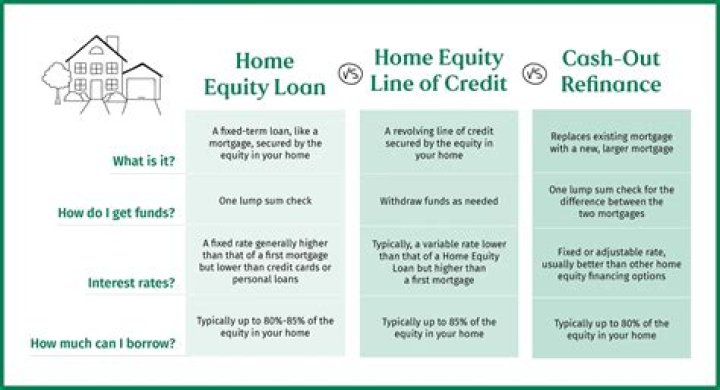

Home Equity Line of Credit for Building a House A construction or home improvement loan is a loan that is separate from the mortgage on your property. On the other hand a home equity loan is a loan that is given against your equity in your home. Or the lender can sell the home.

.

Correspondingly, what is the difference between a construction loan and mortgage?

Key Differences Between Construction Loans and Mortgages Home construction loans are short-term agreements that generally last for a year. Mortgages charge borrowers interest on the entire amount of the loan. Construction loans can provide you with upfront funds to purchase land you wish to build on.

Subsequently, question is, is a construction loan harder to get than a mortgage? Construction loans are very short term, generally with a lifespan of one year or less. Since there is more risk with a construction loan than a standard mortgage, interest rates may be higher. Also, the approval process is different than a regular mortgage.

Similarly, it is asked, what is better mortgage or home equity loan?

The difference between a home equity loan and a traditional mortgage is that you take out a home equity loan after you have equity in the property, while you get a mortgage to purchase the property. Your loan-to-value (LTV) ratio is used by lenders to figure out how much money you can borrow.

Can I use a home equity loan to build a house?

Construction loans are considered higher risk. You will need strong credit and a down payment of 20% to 25%. If you already own the land, you can use it as equity for your construction loan. Your lender will check the credit and credentials of your builder as well.

Related Question AnswersIs it harder to get a construction loan?

They're harder to qualify for: Since construction loans are so flexible, they often come with higher qualifying standards in terms of credit and downpayment. Typically, a score of at least 680 and a down payment of at least 20% is needed.What are typical closing costs for a construction loan?

Here's a breakdown of costs for this type of home: $74,911 for a 20 percent down payment, which is standard for a construction loan. $11,237 for closing costs of 3 percent. $299,643 financed with a mortgage.What happens when you go over budget on construction loan?

If your project goes over budget, you'll need to come up with the difference out of pocket or take out a second loan to cover the overages. For that reason, unless you have a solid grasp of the costs and schedule for the project, a one-time construction loan may not be right for your project.Can I use the value of my land for a downpayment for a construction loan?

Construction lenders normally require the borrower to make a down payment of 30 percent of the loan amount. In some cases, 20 percent will be acceptable. If you own the land where the house will be built, you can use it as equity to secure the loan in lieu of a cash down payment.Is it cheaper to build or buy a house?

If you buy an existing home: According to the latest figures, the median cost of buying an existing single-family house is $223,000. For one, new construction is usually more spacious, with a median size of 2,467 square feet—so the cost to build per square foot, $103, is actually lower than that of existing homes.Can I use my land as collateral to build a house?

If you own you land outright (no mortgage or liens) you can likely use your equity in the land toward the purchase of a new home. In this scenario, you could use your equity in the land as collateral or obtain a nwe loan against property and use the funds as a down payment on building your new home.How much interest will I pay on a construction loan?

Interest on a construction loan is a very simple formula that anyone can calculate. If your current interest rate is 7.75% you simply take the balance that has been drawn or borrowed. You then multiply this balance by . 0775.What are the qualifications for a construction loan?

What Are The Requirements For A Construction Loan- The Lender Needs Detailed Descriptions.

- A Qualified Builder.

- A Down Payment of Minimum 20%.

- Proof of Your Ability to Repay Loan.

- The Property Value Must Be Appraised.

What are the disadvantages of home equity loans?

One of the main disadvantages of home equity loans is that they require the property to be used as collateral, and the lender can foreclose on the property in case the borrower defaults on the loan. This is a risk to consider, but because there is collateral on the loan, the interest rates are typically lower.What are the disadvantages of a home equity line of credit?

Below are three disadvantages you'll want to seriously consider before you commit to a HELOC.- Possible Foreclosure: When a lender grants a home equity line of credit, the borrower's home is secured as collateral.

- Risk of More Debt: Among the biggest problems associated with HELOCs is the potential to rack up more debt.