What is Tbats model?

By Matthew Harrington

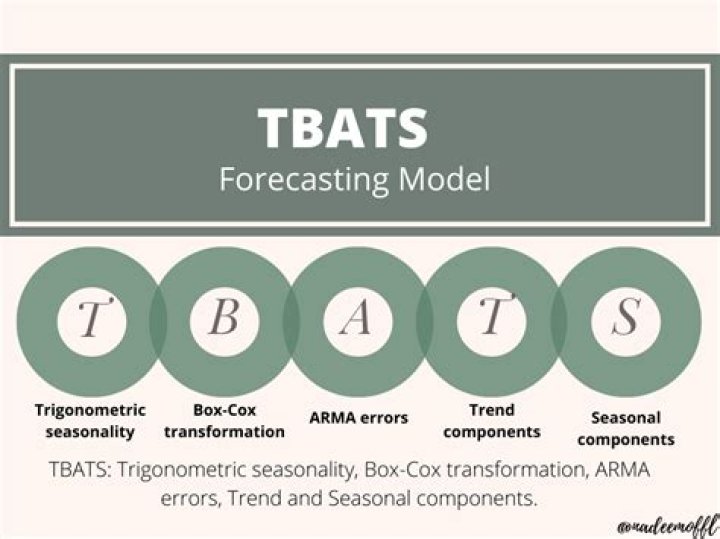

The TBATS model is a time series model for series exhibiting multiple complex seasonalities. The TBATS model was introduced by De Livera, Hyndman & Snyder (2011, JASA). "TBATS" is an acronym denoting its salient features: T for trigonometric regressors to model multiple-seasonalities.

.

Considering this, what is Tbats?

TBATS is modeling yearly seasonal effect. Fig 3: 12 weeks of data. Weekly seasonal effect is also being modeled by TBATS. If we take a look under the hood and review model parameters we will discover that 3 seasonal harmonics are used to model the weekly pattern and 11 harmonics are used to model the yearly pattern.

Similarly, what is exponential smoothing? Exponential smoothing is a rule of thumb technique for smoothing time series data using the exponential window function. Whereas in the simple moving average the past observations are weighted equally, exponential functions are used to assign exponentially decreasing weights over time.

Also to know is, what is ETS model?

SPL is an important factor influencing the dynamics of regional climate and global climate [6]. 2.2. ETS (Error, Trend, Seasonal) ETS (Error, Trend, Seasonal) method is an approach method for forecasting time series univariate. This ETS model focuses on trend and seasonal components [7].

What is seasonality in forecasting?

In statistics, the demand - or the sales - of a given product is said to exhibit seasonality when the underlying time-series undergoes a predictable cyclic variation depending on the time within the year. Seasonality is one of most frequently used statistical patterns to improve the accuracy of demand forecasts.

Related Question AnswersWhat is ETS forecast?

Calculates or predicts a future value based on existing (historical) values by using the AAA version of the Exponential Smoothing (ETS) algorithm. The predicted value is a continuation of the historical values in the specified target date, which should be a continuation of the timeline.What is Arima model in time series?

A popular and widely used statistical method for time series forecasting is the ARIMA model. ARIMA is an acronym that stands for AutoRegressive Integrated Moving Average. It is a class of model that captures a suite of different standard temporal structures in time series data.What does ETS stand for?

expiration – term of serviceWhat is a smoothing factor?

The controlling input of the exponential smoothing calculation is known as the smoothing factor (also called the smoothing constant). It essentially represents the weighting applied to the most recent period's demand.Why do we smooth time series data?

Smoothing is usually done to help us better see patterns, trends for example, in time series. Generally smooth out the irregular roughness to see a clearer signal. For seasonal data, we might smooth out the seasonality so that we can identify the trend.What is Alpha in forecasting?

This forecast rule defines the forecast bucket type, forecast method, and the sources of demand. If the rule is a statistical forecast, the exponential smoothing factor (alpha), trend smoothing factor (beta), and seasonality smoothing factor (gamma) are also part of the rule.What is time series trend?

Web Service. OECD Statistics. Definition: The trend is the component of a time series that represents variations of low frequency in a time series, the high and medium frequency fluctuations having been filtered out.What is exponential smoothing Excel?

Exponential Smoothing is used to forecast the business volume for taking appropriate decisions. This is a way of “Smoothing” out the data by eliminating much of random effects. The idea behind Exponential Smoothing is just to get a more realistic picture of the business by using the Microsoft Excel 2010 and 2013.What is damped trend?

The damped trend method of exponential smoothing is a benchmark that has been difficult to beat in empirical studies of forecast accuracy. One explanation for this success is the flexibility of the method, which contains a variety of special cases that are automatically selected during the fitting process.How do you choose the damping factor for exponential smoothing?

Step 1: Click the “Data” tab and then click “Data Analysis.” Step 2: Select “Exponential Smoothing” and then click “OK.” Step 4: Type a damping factor into the damping factor box. A valid value is 0 to 1.What is exponential trend?

An exponential trendline is a curved line that is most useful when data values rise or fall at increasingly higher rates. You cannot create an exponential trendline if your data contains zero or negative values. Note that the R-squared value is 1, which means the line fits the data perfectly.How is seasonality calculated?

The seasonal index of each value is calculated by dividing the period amount by the average of all periods. This creates a relationship between the period amount and the average that reflects how much a period is higher or lower than the average. =Period Amount / Average Amount or, for example, =B2/$B$15.What does seasonality mean?

Seasonality is a characteristic of a time series in which the data experiences regular and predictable changes that recur every calendar year. Any predictable fluctuation or pattern that recurs or repeats over a one-year period is said to be seasonal.How do you seasonally adjust data?

We call these averages “seasonal factors.” To seasonally adjust your data, divide each data point by the seasonal factor for its month. If January's average ratio is 0.85, it means that January runs about 15 percent below normal.How does forecast work in Excel?

The FORECAST function in Excel is used to predict a future value by using linear regression. In other words, FORECAST projects a future value along a line of best fit based on historical data. Where: X (required) - a numerical x-value for which you want to predict a new y-value.What is Deseasonalized data?

Econometrics For Dummies In many cases, seasonal patterns are removed from time-series data when they're released on public databases. Data that has been stripped of its seasonal patterns is referred to as seasonally adjusted or deseasonalized data.How do you forecast time series data in Excel?

Create a forecast- In a worksheet, enter two data series that correspond to each other:

- Select both data series.

- On the Data tab, in the Forecast group, click Forecast Sheet.

- In the Create Forecast Worksheet box, pick either a line chart or a column chart for the visual representation of the forecast.

How do I use Excel to forecast historical data?

Follow the steps below to use this feature.- Select the data that contains timeline series and values.

- Go to Data > Forecast > Forecast Sheet.

- Choose a chart type (we recommend using a line or column chart).

- Pick an end date for forecasting.

- Click the Create.