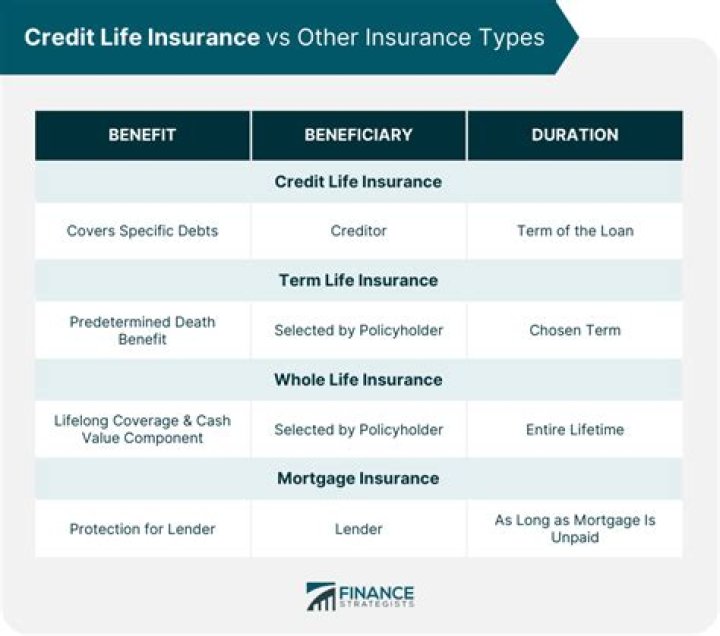

Credit life insurance is a type of life insurance policy designed to pay off a borrower's outstanding debts if the borrower dies. The face value of a credit life insurance policy decreases proportionately with the outstanding loan amount as the loan is paid off over time, until both reach zero value..

Also, is credit life insurance a good idea?

Some lenders require credit life In some cases, a lender may require a borrower to take out a credit life insurance policy. Lynch says it's a good idea to find appropriate life insurance coverage so that your loved ones will be able to make the mortgage payments if something happens to you.

Additionally, what is credit insurance and how does it work? Credit insurance is an insurance policy that pays off an outstanding debt in the event of the policy holder's death, disability, or termination of employment. When a company obtains credit insurance — called trade credit insurance — it provides protection against customer insolvency.

Secondly, is there an age limit for credit life insurance?

Generally, a lender may not require a borrower to buy credit life insurance as a condition for being approved for a loan. There is no universal rule concerning age limitations on credit life insurance contracts. Some policies end when the borrower reaches the age of 70. However, this is not a hard-and-fast rule.

How much is credit life insurance on a mortgage?

Price Compared to Term According to Wisconsin's Department of Financial Institutions, a healthy 40-year-old man with a $50,000 loan will pay as much as $370 per year for credit life insurance on that loan, but will pay as little as $92 per year for a $50,000 term life insurance policy.

Related Question Answers

Do credit cards offer life insurance?

Four Main Types of Credit Insurance: Credit life insurance pays off the debt you owe if you die. The beneficiary of the policy is the credit card company. If you have life insurance that is enough to pay off your debts if you die, consider this before spending more money on this extra coverage.What insurance pays off your car if you die?

Credit life insurance is a type of life insurance policy designed to pay off a borrower's outstanding debts if the borrower dies.How much does credit insurance cost?

The U.S. Government Accountability Office found premiums for credit insurance on credit card balances ranged from 85 cents to $1.35 a month per $100 of outstanding balance. On a $5,000 balance, that insurance could cost $44 to $67 a month.How much is life insurance on a car?

The average cost of credit life insurance is about $. 50 for every $100 borrowed. Let's say that you took out a $20,000 auto loan for five years. This means you are paying $100 per year for protection on a loan for which the benefits do not go to anyone else but the lender.What is credit life and disability protection?

Credit insurance is a term which applies to 4 different types of policy: Credit life insurance - Pays off a debt if you pass away. Credit disability insurance - Covers loan payments if you become disabled and unable to work. Credit property insurance - Covers property used to secure a loan, such as a boat or car.What is a credit insurance policy?

Credit Insurance Defined. By Julia Kagan. Updated Jan 20, 2018. Credit insurance is a type of insurance policy purchased by a borrower that pays off one or more existing debts in the event of a death, disability, or in rare cases, unemployment.Does PMI pay off your mortgage if you die?

PMI stands for private mortgage insurance. However, PMI doesn't pay off your loan if you die. In fact, it is intended more as a protection for your lender if you don't repay your debt. Mortgage protection insurance is an option if you want this type of death benefit.What is insurance on a loan?

Loan protection insurance is designed to help policyholders by providing financial support in times of need. Whether the need is due to disability or unemployment, this insurance can help cover monthly loan payments and protect the insured from default.Is my mortgage paid off if I die?

If you died, the lender would receive a check to pay off whatever remained on the mortgage. The downside is that the value of the policy decreases every year, because it will only pay whatever you still owe on the loan. And the money goes directly to the mortgage lender, not to your heirs.What happens to mortgage when you die?

When the homeowner dies before the mortgage loan is fully paid, the lender is still holding its security interest in the property. If someone doesn't pay off the mortgage, the bank can foreclose on the property and sell it in order to recoup its money.What credit life insurance covers?

'Credit life insurance' is the insurance cover a consumer takes out in the event of their death, disability, terminal illness, unemployment, or other insurable risk that is likely to impair the consumer's ability to earn an income or pay their monthly instalments under a credit agreement.What happens to my car payment if I die?

When someone dies, the family has many important issues to manage. Unfortunately, debts are eventually among those issues. The lender of a car loan can repossess a vehicle if payments stop. The loan becomes a debt owed by the estate of the deceased person just like other debts, such as credit or mortgage obligations.What is a 10 pay life policy?

10 Pay whole life insurance is a whole life product that becomes contractually paid up after ten years of payments. The policy only requires that the policyholder pay premiums for 10 years. Dividends paid to 10 pay whole life insurance policies come in the same fashion any whole life dividend comes.Who is considered the debtor in a credit disability insurance policy?

(4) “Debtor” means a borrower of money or a purchaser or lessee of goods, services, property, rights or privileges for which payment is arranged through a credit transaction.What type of insurance is known as Consumer Credit Insurance?

Consumer credit insurance is also known as CCI or credit, loan or mortgage protection insurance. Consumer credit insurance offers poor value and is not compulsory. Before you sign up, work out if it offers you any value for money.What is credit life insurance on a car?

What is credit insurance for an auto loan? Credit insurance is optional insurance that make your auto payments to your lender in certain situations, such as if you die or become disabled.What is level term life insurance?

Level-premium insurance is term life insurance for which the premiums are guaranteed to remain the same throughout the contract, while the amount of coverage provided increases. Level-Premium is different from term life insurance policies, as they have premium rates that rise as the policies age.How does credit guarantee work?

A credit guarantee scheme provides third-party credit risk mitigation to lenders through the absorption of a portion of the lender's losses on the loans made to SMEs in case of default, typically in return for a fee.How does credit card insurance work?

Credit Card Insurance, sometimes known as balance protection insurance, pays out your outstanding balance (subject to any limits in the policy) or makes monthly payments on your behalf to your credit card issuer if your income is interrupted by unforeseen events.