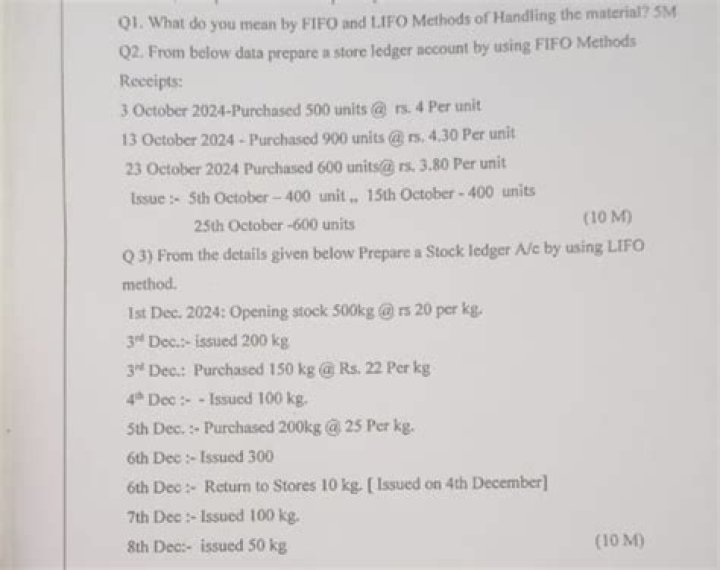

FIFO and LIFO are cost layering methods used to value the cost of goods sold and ending inventory. LIFO is a contraction of the term "last in, first out," and means that the goods last added to inventory are assumed to be the first goods removed from inventory for sale..

People also ask, what is difference between LIFO and FIFO?

Key Differences Between LIFO and FIFO In LIFO, the stock in hand represents, oldest stock while in FIFO, the stock in hand is the latest lot of goods. In LIFO, the cost of goods sold (COGS) shows current market price while in the case of FIFO the cost of unsold stock shows current market price.

Likewise, what do you mean by FIFO method? First-In, First-Out

Beside above, what is LIFO and FIFO with example?

FIFO (“First-In, First-Out”) assumes that the oldest products in a company's inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company's inventory have been sold first and uses those costs instead.

What do you mean by LIFO?

Last In, First Out

Related Question Answers

What are the advantages of FIFO?

Advantages and disadvantages of FIFO The FIFO method has four major advantages: (1) it is easy to apply, (2) the assumed flow of costs corresponds with the normal physical flow of goods, (3) no manipulation of income is possible, and (4) the balance sheet amount for inventory is likely to approximate the current marketWhat is LIFO used for?

LIFO stands for “Last-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The LIFO method assumes that the most recent products added to a company's inventory have been sold first. The costs paid for those recent products are the ones used in the calculation.How is FIFO calculated?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.Why LIFO is not allowed?

One of the reason that LIFO is not allowed because reduction in tax burden under inflationary economies. This can happen because LIFO assumes that inventory will be consumed in the production process. The main reason for excluding the LIFO is because IFRS shifted its focus on balance sheet instead of income statement.What is mean by LIFO?

Last In, First Out

What is FIFO and LIFO example?

FIFO (“First-In, First-Out”) assumes that the oldest products in a company's inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company's inventory have been sold first and uses those costs instead.What is an example of FIFO?

Example of FIFO For example, if 100 items were purchased for $10 and 100 more items were purchased next for $15, FIFO would assign the cost of the first item resold of $10. After 100 items were sold, the new cost of the item would become $15, regardless of any additional inventory purchases made.What is LIFO example?

LIFO stands for “Last-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The LIFO method assumes that the most recent products added to a company's inventory have been sold first. The costs paid for those recent products are the ones used in the calculation.Where is LIFO used?

The LIFO method is used in the COGS (Cost of Goods Sold) calculation when the costs of producing a product or acquiring inventory has been increasing. This may be due to inflation.What is FIFO example?

Example of FIFO For example, if 100 items were purchased for $10 and 100 more items were purchased next for $15, FIFO would assign the cost of the first item resold of $10. After 100 items were sold, the new cost of the item would become $15, regardless of any additional inventory purchases made.Why FIFO is used?

The FIFO and LIFO Methods are accounting techniques used in managing a company's stock and financial matters. They help a company determine the value of their stock, raw materials, etc. They are used to manage cost flows assumptions related to stock and stock repurchases (if purchased at different prices).What is the FIFO process?

In other words, FIFO is a method of inventory valuation based on the assumption that goods are sold or used in the same chronological order in which they are bought. FIFO describes the principle of a queue processing technique or servicing conflicting demands by ordering process by first come, first serve behavior.What happens when prices are falling LIFO?

What happens when prices are falling? LIFO will result in lower net income and a lower inventory valuation than will FIFO LIFO will result in higher net income and a higher inventory valuation than will FIFO LIFO will result in higher net income and a lower inventory valuation than will FIFO.Why FIFO is better?

If the opposite its true, and your inventory costs are going down, FIFO costing might be better. Since prices usually increase, most businesses prefer to use LIFO costing. If you want a more accurate cost, FIFO is better, because it assumes that older less-costly items are most usually sold first.