Is paying student loans tax-deductible?

By Daniel Johnston

Is paying student loans tax-deductible?

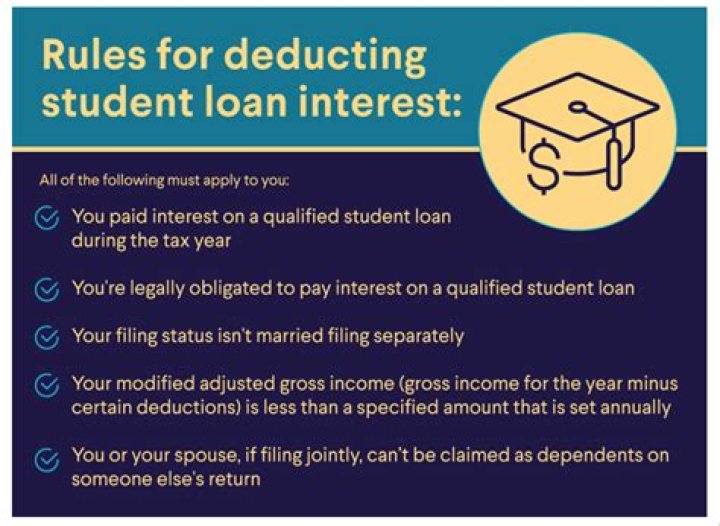

Student Loan Interest Deduction You can take a tax deduction for the interest paid on student loans that you took out for yourself, your spouse, or your dependent. This benefit applies to all loans (not just federal student loans) used to pay for higher education expenses. The maximum deduction is $2,500 a year.

Are student loan payments tax-deductible 2020?

And while you can’t deduct a student loan on your federal tax return, the interest from student loan payments is tax-deductible. The student loan interest deduction allows you to deduct up to $2,500 on your federal income tax return for the loan interest you paid during the year.

Are student loan payments tax-deductible 2019?

If you have qualifying student loan debt, you can deduct the interest you paid on the loan during the tax year. This is capped at $2,500 in total interest per return, not per person, each year. In other words, if you’re single, you can deduct as much as $2,500 of student loan interest.

How much of my student loan interest is tax deductible?

You may deduct the lesser of $2,500 or the amount of interest you actually paid during the year. The deduction is gradually reduced and eventually eliminated by phaseout when your modified adjusted gross income (MAGI) amount reaches the annual limit for your filing status.

Is it worth it to claim student loan interest?

The Student Loan Interest Deduction May Not Be Worth The Paper It’s Printed On. Although this is an above-the-line deduction in that it reduces your gross income directly to compute adjusted gross income (you don’t need to itemize), there are several restrictions that limit any actual tax benefits.

How do I claim student loan interest on taxes?

You can claim the interest you paid on your student loan via Line 31900 of your tax return. On that line, you can input the amount of interest paid. You might be eligible for a student loan interest tax credit if your income tax was higher than the credit amount.

What is the income limit for student loan interest deduction?

Is student loan interest deductible? Student loan interest is deductible if your modified adjusted gross income, or MAGI, is less than $70,000 ($140,000 if filing jointly). If your MAGI was between $70,000 and $85,000 ($170,000 if filing jointly), you can deduct less than than the maximum $2,500.

Will I get my tax refund if I owe student loans 2022?

If you default on a federal student loan, your tax refunds can be taken to help cover what you owe. However, the government has paused this program and other collection activities through Jan. 31, 2022, due to the pandemic.

Can student loans take my tax refund during Covid 19?

Normally, if your student loans are in default status, your tax return will be seized to cover some of the defaulted balance. However, in 2020, the federal government halted all student loans collections, which means that tax returns weren’t offset.

How much do you get back in taxes for paying student loans?

The Internal Revenue Service (IRS) outlines a variety of tax deductions that allow individuals to reduce their taxable income for the year. One of these is the student loan interest deduction, which allows for the deduction of up to $2,500 of the interest paid on a student loan during the tax year.

Do student loans affect your tax refund?

You must have federal student loans in default to have your tax refund garnished. Federal student loans enter default after 270 days of past-due payments. Private student loans in default aren’t eligible for tax refund garnishment.