How much is the monthly mortgage insurance for FHA?

By Sophia Dalton

FHA MIP Chart

| FHA MIP Chart for Loans Greater Than 15 Years | ||

|---|---|---|

| Base Loan Amount | LTV | Annual MIP |

| ≤$625,500 | ≤95.00% | 0.80% |

| ≤$625,500 | >95.00% | 0.85% |

| >$625,500 | ≤95.00% | 1.00% |

.

Furthermore, how long is mortgage insurance required for FHA?

Depending on your down payment, and when you first took out the loan, FHA mortgage insurance premium (MIP) usually lasts 11 years or the life of the loan. MIP will not fall off automatically. To remove MIP from an FHA loan, you'll have to refinance into another mortgage program once you reach 20% equity.

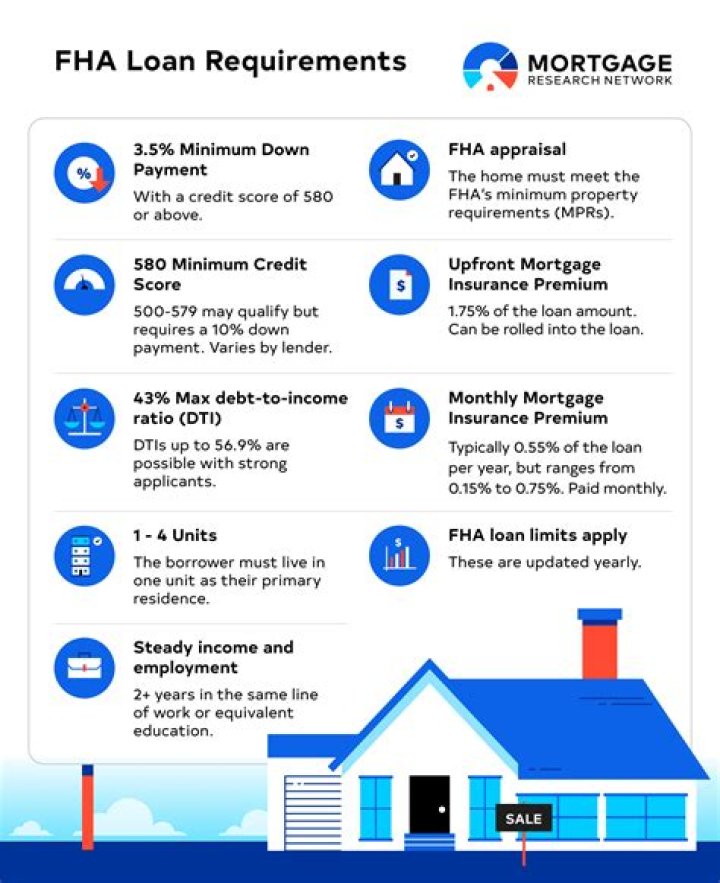

Subsequently, question is, does an FHA loan require mortgage insurance? Mortgage insurance is required on most loans when borrowers put down less than 20 percent. All FHA loans require the borrower to pay two mortgage insurance premiums: Upfront mortgage insurance premium: 1.75 percent of the loan amount, paid when the borrower gets the loan.

Keeping this in view, how is FHA monthly mortgage insurance calculated?

The monthly insurance premium, or MIP, is 0.50 percent of the loan amount. Multiply the loan amount by 0.50 percent, and divide the sum by 12. $197,342.50 multiplied by 0.005 is $986.71; $986.71 divided by 12 equals $82.23. The actual number is 82.226, but the FHA requires rounding to the nearest cent.

What is the monthly FHA MIP factor?

At a glance: Most FHA borrowers pay an annual MIP of 0.85% for the full term of the loan, or up to 30 years.

FHA Loans Greater Than 15 Years.

| Base Loan Amt. | LTV | Annual MIP |

|---|---|---|

| ≤$625,500 | ≤95.00% | 80 bps (0.80%) |

| ≤$625,500 | >95.00% | 85 bps (0.85%) |

| >$625,500 | ≤95.00% | 100 bps (1.00%) |

| >$625,500 | >95.00% | 105 bps (1.05%) |

Is an FHA loan bad?

Since the FHA insures these loans, that means if borrowers default on the loan, the government will pay the lender for any losses. FHA-backed loans usually have more lenient requirements than conventional loans—lower credit scores are required and your down payment can be as low as 3.5 percent.Can I remove FHA mortgage insurance?

You can remove PMI after 11 years if you put more than 10% down. The FHA no longer allows borrowers to cancel FHA MIP after the LTV has reached 78%. You can still avoid paying mortgage insurance after you have paid down your loan-to-value to 80% or less, such as refinancing your FHA loan to a conventional loan.How do I avoid private mortgage insurance?

One way to avoid paying PMI is to make a down payment that is equal to at least one-fifth of the purchase price of the home; in mortgage-speak, the mortgage's loan-to-value (LTV) ratio is 80%. If your new home costs $180,000, for example, you would need to put down at least $36,000 to avoid paying PMI.Should I refinance to get rid of FHA PMI?

Refinance the Mortgage This will work if your new mortgage is for 80% or less of the home's current appraised value. You'll most likely need an appraisal to refinance your mortgage, anyway. Refinancing is the only option for getting rid of PMI on most government-backed loans, such as FHA loans.Does PMI fall off FHA loan?

And though FHA doesn't require PMI, it does require that borrowers help to fund its unique MIP-based mortgage insurance version. On 30-year loans, FHA borrowers' MIP payments are automatically stopped after five years, but only if their properties reach 78 percent loan-to-value (LTV).What credit score do I need for an FHA loan?

For those interested in applying for an FHA loan, applicants are now required to have a minimum FICO score of 580 to qualify for the low down payment advantage, which is currently at around 3.5 percent. If your credit score is below 580, however, you aren't necessarily excluded from FHA loan eligibility.Who qualifies for FHA loans?

How To Qualify For An FHA Loan- Have verifiable income.

- Be able to afford the housing payment AND any existing debt.

- Save at least a 3.5 percent down payment.

- Have an established credit history.

- Have a FICO score of at least 580-640.

- Purchase a home that does not exceed FHA loan limits.

- Apply for the correct type of FHA loan.

How does FHA insurance work?

FHA Mortgage Insurance Premium (MIP), like PMI, is an additional fee you pay to protect the lender's financial interests in case you default on your loan. FHA borrowers are required to pay two FHA mortgage insurance premiums — upfront at closing, and annually for as long as you repay your FHA loan, in most cases.How do I avoid upfront mortgage insurance premium?

There are a few ways home buyers can avoid paying upfront mortgage insurance:- Apply for a conventional mortgage loan. Mortgage lenders will not require upfront mortgage insurance for conventional loans that have an 80% loan to value or less.

- Make a 20% down payment.

- Get a second mortgage.

- Get help from the seller.

How is mortgage insurance calculated?

The PMI formula is actually simpler than a fixed-rate mortgage formula.- Find out the loan-to-value, or LTV, ratio of your house.

- 450,000 / 500,000 = 0.9.

- 0.9 X 100 = 90 percent LTV.

- Look at the lender's PMI table.

- Multiply your mortgage loan by your specific PMI rate according to the lender's chart.

Does FHA MIP decrease annually?

FHA has varying rates on annual MIP, depending on the size of the loan and the amount of the down payment. As the loan balance declines, the annual MIP premium will decline with it. Still, the reduction in the premium rate could save you a load of money over the life of your loan.How is monthly mortgage insurance premium calculated?

Calculating Your Costs To calculate the rate, takes the rate of insurance and multiply it by the value of the loan. For example, assuming a 1 percent MIP on a $200,000 loan with only 5 percent down payment – $195,000 loan value – results in $1,950 annual MIP payments or $162.50 added to your monthly payments.What is mortgage insurance premium?

Mortgage insurance is paid if you as a borrower were to make a down payment of less than 20 percent on your home loan. It is paid by you, but is used to protect the lender from losses if you were to default on the loan. When it comes to the FHA, borrowers must pay a mortgage insurance premium, or MIP, on the home loan.What is FHA funding fee?

The current FHA Upfront Funding Fee is 2.25 percent of your new mortgage amount. You can simply multiply your mortgage amount by the prevailing fee percentage to calculate your Upfront Funding Fee.What is the upfront MIP for FHA loans?

FHA Upfront MIP. MIP stands for mortgage insurance premium and is required to close an FHA loan. It is paid as an upfront cost and as an annual premium. PMI is required on conventional loans with a down payment of less than 20 percent to protect the lender in case the borrower were to default on the loan.What is the income limit for FHA loan?

Short answer: The general rule for FHA loans is 43% debt-to-income ratio. This means your combined debts should use no more than 43% of your gross monthly income — after taking on the loan. But there are exceptions.Should I get an FHA loan or conventional?

Conventional loans generally require that you have a FICO credit score of at least 620 to qualify, and a higher credit score is needed to qualify for the best interest rates. You can get an FHA loan with a down payment as low as 3.5 percent.Loan limits.

| FHA | Conventional | |

|---|---|---|

| 4 unit | $566,425 | $871,450 |