How do you interpret autocorrelation results?

By Sarah Smith

How do you interpret autocorrelation results?

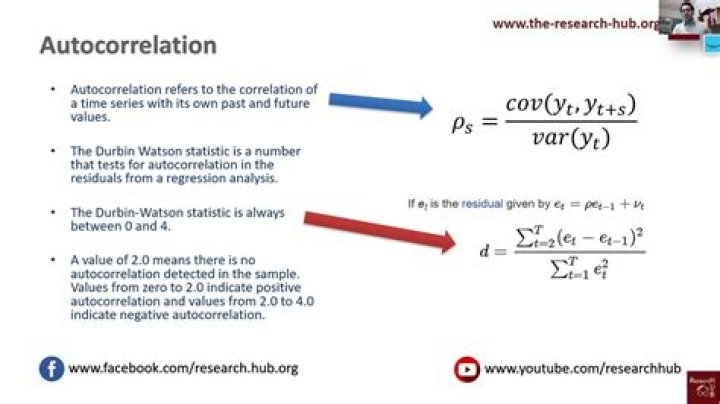

Autocorrelation measures the relationship between a variable’s current value and its past values. An autocorrelation of +1 represents a perfect positive correlation, while an autocorrelation of negative 1 represents a perfect negative correlation.

What do ACF plots tell us?

We have an ACF plot. In simple terms, it describes how well the present value of the series is related with its past values. A time series can have components like trend, seasonality, cyclic and residual. ACF considers all these components while finding correlations hence it’s a ‘complete auto-correlation plot’.

How do you interpret partial autocorrelation?

The partial autocorrelation function is a measure of the correlation between observations of a time series that are separated by k time units (y t and y t–k), after adjusting for the presence of all the other terms of shorter lag (y t–1, y t–2., y t–k–1).

How much autocorrelation is acceptable?

A value of 2 or nearly 2 indicates that there is no first-order autocorrelation. An acceptable range is 1.50 – 2.50.

What are correlations in statistics?

Correlation is a statistical measure that expresses the extent to which two variables are linearly related (meaning they change together at a constant rate). It’s a common tool for describing simple relationships without making a statement about cause and effect.

What is autocorrelation analysis?

Autocorrelation analysis measures the relationship of the observations between the different points in time, and thus seeks for a pattern or trend over the time series. For example, the temperatures on different days in a month are autocorrelated.

What does a negative ACF mean?

Negative ACF means that a positive oil return for one observation increases the probability of having a negative oil return for another observation (depending on the lag) and vice-versa.

What is ARIMA PDQ?

A nonseasonal ARIMA model is classified as an “ARIMA(p,d,q)” model, where: p is the number of autoregressive terms, d is the number of nonseasonal differences needed for stationarity, and. q is the number of lagged forecast errors in the prediction equation.

How do you interpret PACF and ACF plots?

Identifying AR and MA orders by ACF and PACF plots: To define a MA process, we expect the opposite from the ACF and PACF plots, meaning that: the ACF should show a sharp drop after a certain q number of lags while PACF should show a geometric or gradual decreasing trend.

What is a good Durbin-Watson value?

A rule of thumb is that DW test statistic values in the range of 1.5 to 2.5 are relatively normal. Values outside this range could, however, be a cause for concern. The Durbin–Watson statistic, while displayed by many regression analysis programs, is not applicable in certain situations.