How do you calculate covariance from variance?

By John Johnson

How to Calculate Variance. Variance is calculated by taking the differences between each number in a data set and the mean, squaring those differences to give them positive value, and dividing the sum of the resulting squares by the number of values in the set.

.

Keeping this in view, how is covariance related to variance?

Variance and covariance are mathematical terms frequently used in statistics and probability theory. Variance refers to the spread of a data set around its mean value, while a covariance refers to the measure of the directional relationship between two random variables.

how do you find the variance covariance matrix? Here's how.

- Transform the raw scores from matrix X into deviation scores for matrix x. x = X - 11'X ( 1 / n )

- Compute x'x, the k x k deviation sums of squares and cross products matrix for x.

- Then, divide each term in the deviation sums of squares and cross product matrix by n to create the variance-covariance matrix.

Similarly, it is asked, what is the formula of covariance?

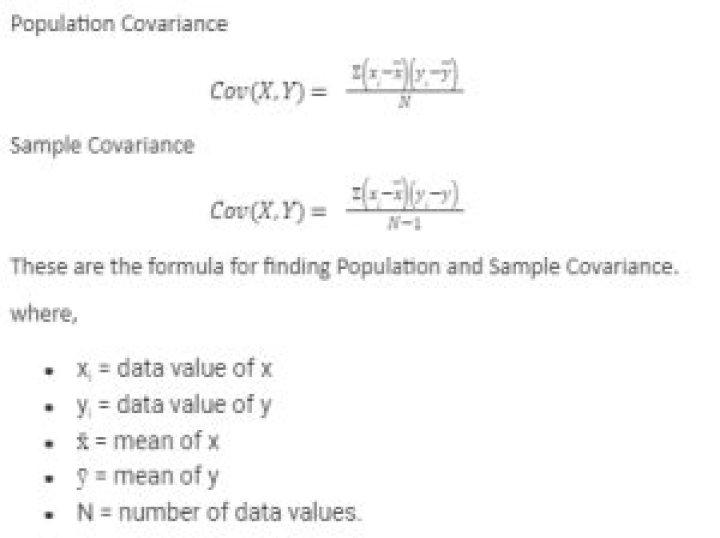

Covariance indicates how two variables are related. A positive covariance means the variables are positively related, while a negative covariance means the variables are inversely related. The formula for calculating covariance of sample data is shown below. x = the independent variable. y = the dependent variable.

How do you explain variance?

Variance is calculated by taking the differences between each number in the data set and the mean, then squaring the differences to make them positive, and finally dividing the sum of the squares by the number of values in the data set.

Related Question AnswersWhy is variance important?

It is extremely important as a means to visualise and understand the data being considered. Statistics in a sense were created to represent the data in two or three numbers. The variance is a measure of how dispersed or spread out the set is, something that the “average” (mean or median) is not designed to do.Can the variance be negative?

Negative Variance Means You Have Made an Error As a result of its calculation and mathematical meaning, variance can never be negative, because it is the average squared deviation from the mean and: Anything squared is never negative. Average of non-negative numbers can't be negative either.Why do we use covariance?

Covariance is a statistical tool that is used to determine the relationship between the movement of two asset prices. When two stocks tend to move together, they are seen as having a positive covariance; when they move inversely, the covariance is negative.What affects variance?

Factors affecting power: Variance (1 of 2) The larger the variance (σ²), the lower the power. increasing σ² increases the denominator and therefore lowers z and power. For the example, σ is the standard deviation of the difference scores. The power of the test using the .What is the difference between correlation and variance?

You only know the magnitude here, as in how much the data is spread. Covariance tells us direction in which two quantities vary with each other. Correlation shows us both, the direction and magnitude of how two quantities vary with each other. Variance is fairly simple.What does COV XY mean?

Definition. Let X and Y be random variables (discrete or continuous!) with means μX and μY. The covariance of X and Y, denoted Cov(X,Y) or σXY, is defined as: Cov(X,Y)=sigma_{XY}=E[(X-mu_X)(Y-mu_Y)]What is the meaning of covariance in statistics?

In probability theory and statistics, covariance is a measure of the joint variability of two random variables. In the opposite case, when the greater values of one variable mainly correspond to the lesser values of the other, (i.e., the variables tend to show opposite behavior), the covariance is negative.What does a covariance of 0 mean?

Zero covariance - if the two random variables are independent, the covariance will be zero. However, a covariance of zero does not necessarily mean that the variables are independent. A nonlinear relationship can exist that still would result in a covariance value of zero.What does a covariance of 1 mean?

Covariance is a measure of how changes in one variable are associated with changes in a second variable. Specifically, covariance measures the degree to which two variables are linearly associated. However, it is also often used informally as a general measure of how monotonically related two variables are.What is the symbol for mean?

The symbol 'μ' represents the population mean. The symbol 'Σ Xi' represents the sum of all scores present in the population (say, in this case) X1 X2 X3 and so on. The symbol 'N' represents the total number of individuals or cases in the population. Population Standard Deviation.What is a high covariance?

Covariance in Excel: Overview Covariance gives you a positive number if the variables are positively related. You'll get a negative number if they are negatively related. A high covariance basically indicates there is a strong relationship between the variables. A low value means there is a weak relationship.What COV means?

coefficient of variationIs covariance always positive?

The correlation coefficient is equal to the covariance divided by the product of the standard deviations of the variables. Therefore, a positive covariance always results in a positive correlation and a negative covariance always results in a negative correlation.Is covariance the same as standard deviation?

In probability theory and statistics, the mathematical concepts of covariance and correlation are very similar. If Y always takes on the same values as X, we have the covariance of a variable with itself (i.e. ), which is called the variance and is more commonly denoted as the square of the standard deviation.How do you find SD?

To calculate the standard deviation of those numbers:- Work out the Mean (the simple average of the numbers)

- Then for each number: subtract the Mean and square the result.

- Then work out the mean of those squared differences.

- Take the square root of that and we are done!