In finance, a swap is a derivative contract in which one party exchanges or swaps the values or cash flows of one asset for another. Swaps are customized contracts traded in the over-the-counter (OTC) market privately, versus options and futures traded on a public exchange..

Beside this, how are interest swaps traded?

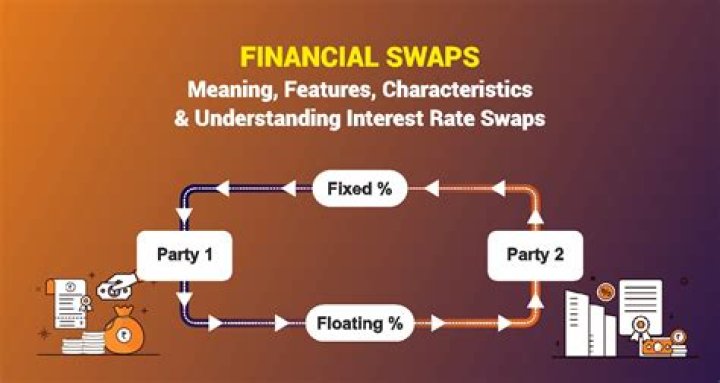

An interest rate swap is an interest rate derivative product that trades over the counter (OTC). It is an agreement between two parties to exchange one stream of interest payments for a different stream, over a certain period of time. Most interest rate products have a “fixed leg” and a “floating leg”.

Secondly, how does a swap work? A swap is an agreement for a financial exchange in which one of the two parties promises to make, with an established frequency, a series of payments, in exchange for receiving another set of payments from the other party. These flows normally respond to interest payments based on the nominal amount of the swap.

In this way, how are equity swaps traded?

An equity swap is an exchange of future cash flows between two parties that allows each party to diversify its income for a specified period of time while still holding its original assets. Swaps trade over-the-counter and are very customizable, based on what two parties agree to.

Why are swaps used?

Swapping allows companies to revise their debt conditions to take advantage of current or expected future market conditions. Currency and interest rate swaps are used as financial tools to lower the amount needed to service a debt as a result of these advantages.

Related Question Answers

How do you price swaps?

To price a swap, we need to determine the present value of cash flows of each leg of the transaction. In an interest rate swap, the fixed leg is fairly straightforward since the cash flows are specified by the coupon rate set at the time of the agreement.Who uses interest rate swaps?

An interest rate swap is a financial derivative that companies use to exchange interest rate payments with each other. Swaps are useful when one company wants to receive a payment with a variable interest rate, while the other wants to limit future risk by receiving a fixed-rate payment instead.What is a vanilla swap?

The most common and simplest swap is a "plain vanilla" interest rate swap. In this swap, Party A agrees to pay Party B a predetermined, fixed rate of interest on a notional principal on specific dates for a specified period of time. In a plain vanilla swap, the two cash flows are paid in the same currency.What is Swap stand for?

size, weight and power

What is a 5 year swap rate?

For example, if the current market rate for a 5-year treasury swap is 1.410% and the current 5-year Treasury yield is 1.420%, the 5-year swap spread would be -0.01%.What are the types of swaps?

The generic types of swaps, in order of their quantitative importance, are: interest rate swaps, basis swaps, currency swaps, inflation swaps, credit default swaps, commodity swaps and equity swaps.What type of hedge is an interest rate swap?

Interest rate swaps allow companies to exchange interest payments on an agreed notional amount for an agreed period of time. Swaps may be used to hedge against adverse interest rate movements or to achieve a desired balanced between fixed and variable rate debt.Is an interest rate swap a derivative?

An interest rate swap is an agreement between two parties to exchange one stream of interest payments for another, over a set period of time. Swaps are derivative contracts and trade over-the-counter. LIBOR is the benchmark for floating short-term interest rates and is set daily.Are swaps a zero sum game?

Swaps are what we call a zero-sum game – gains to one side are offset by the losses to the counterparty. The primary risk statistics (i.e., duration in its various forms) for an interest rate swap are calculated by interpreting the derivative as a “long- short” combination of a fixed-rate and a floating-rate bond.What is a bullet swap?

A bullet swap is like a total return swap except that it defers payment until the swap matures or your position is closed. This means that no cash exchanges hands on reset. When you do, Geneva lets you override financing on the deferred cash flows for dividends, interest, and trade proceeds (realized gains/losses).How many legs does a swap have?

In the simplest vanilla interest rate swap, there are two legs, one with a fixed rate and the other a floating rate. Many other more complex swaps can also be represented.What is the difference between equity swap and total return swap?

Total Return Equity Swap. Similar to a total return swap on a bond, it is a 2-sided financial contract in that one counterparty pays out the total return of the equity, including its dividends and capital appreciation or depreciation, and in return, receives a regular fixed or floating cash flow.What is equity swap with example?

In an equity swap, two parties agree to exchange a set of future cash flows periodically for s specified period of time. The cash flows on the other leg are linked to the returns from a stock or a stock index. The leg linked to the stock or the stock index is referred to as the equity leg of the swap.How does total return swap work?

A total return swap is a swap agreement in which one party makes payments based on a set rate, either fixed or variable, while the other party makes payments based on the return of an underlying asset, which includes both the income it generates and any capital gains.Is an equity swap a derivative?

An equity swap is a financial derivative contract (a swap) where a set of future cash flows are agreed to be exchanged between two counterparties at set dates in the future. The two cash flows are usually referred to as "legs" of the swap; one of these "legs" is usually pegged to a floating rate such as LIBOR.What is a swap reset?

Swap Reset. The mechanism by which an interest rate swap with floating rates based on LIBOR typically resets at fixed intervals (such as three months or six months). An interest rate swap with a 3-month LIBOR leg will have this leg reset every three months to reflect changes in interest rate markets.What is a swap order?

Swap Order. For example, an investor may make a swap order to buy a certain number of shares of Stock X and sell the same number of shares, but only if the broker can sell them at $1 more per share. If the broker is unable to do this, then no part of the order is executed. A swap order is also called a switch order.What is swap value?

An interest rate swap is a contractual agreement between two parties agreeing to exchange cash flows of an underlying asset for a fixed period of time. This value changes over time, however, due to changes in factors affecting the value of the underlying rates.How do you value cross currency swaps?

The CCS is valued by discounting the future cash flows for both legs at the market interest rate applicable at that time. The sum of the cash flows denoted in the foreign currency (hereafter euro) is converted with the spot rate applicable at that time.